[vc_row][vc_column][vc_column_text]

Part 3 to Part VI Form 4562 Depreciation and Amortization

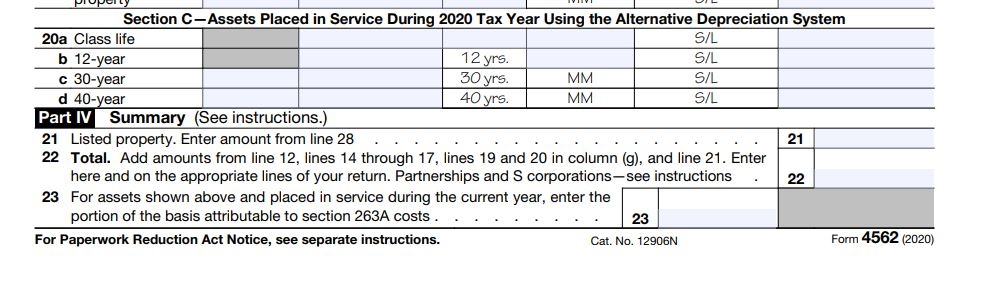

If you choose or are required to use the alternative depreciation system ADS, use section C line 20 a to line 20 d from column a to g to depreciate your asset. Unless it is required, you should depreciate your business asset under the General Depreciation System.

Part IV Summary

Line 21: enter the depreciated amount from line 28 for listed property.

Line 22: for partnerships and S corporation, do not include amount from line 12 section 179 here. Add it to appropriate line on schedule k-1 for the partners. It is a past through entity.

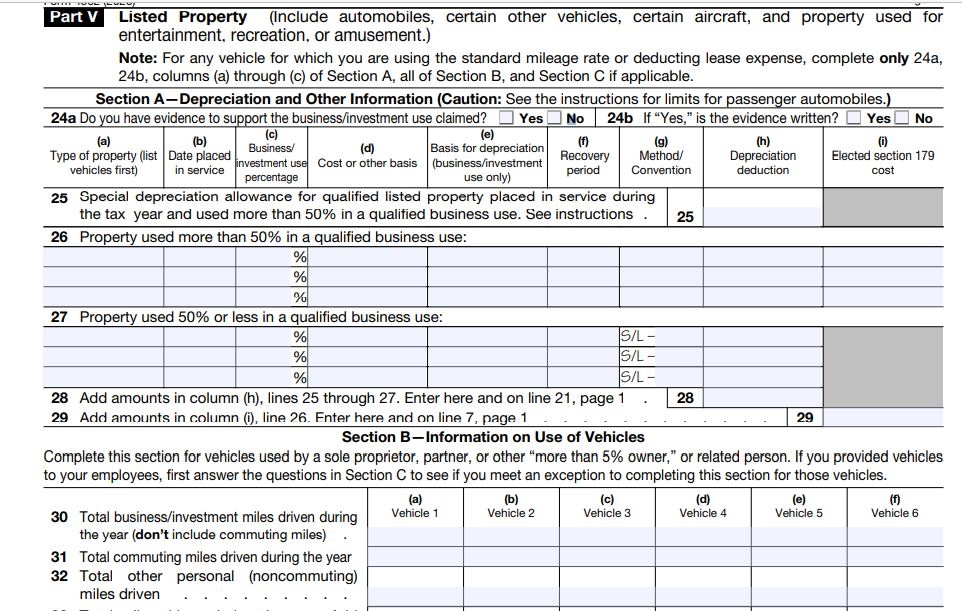

Part V Listed Property

A listed property is a property used for personal and business purposes.

Line 24 a: check the box Yes if you have support document on how you use the property for personal and business

Line 24 b: click yes if you have written record

Line 26 is for listed property used more than 50% in your business while Line 27 is for listed property used for business 50% or less.

Column d is for the cost or the basis of the property at the time you started to use it in your business

Column e is column d * column c

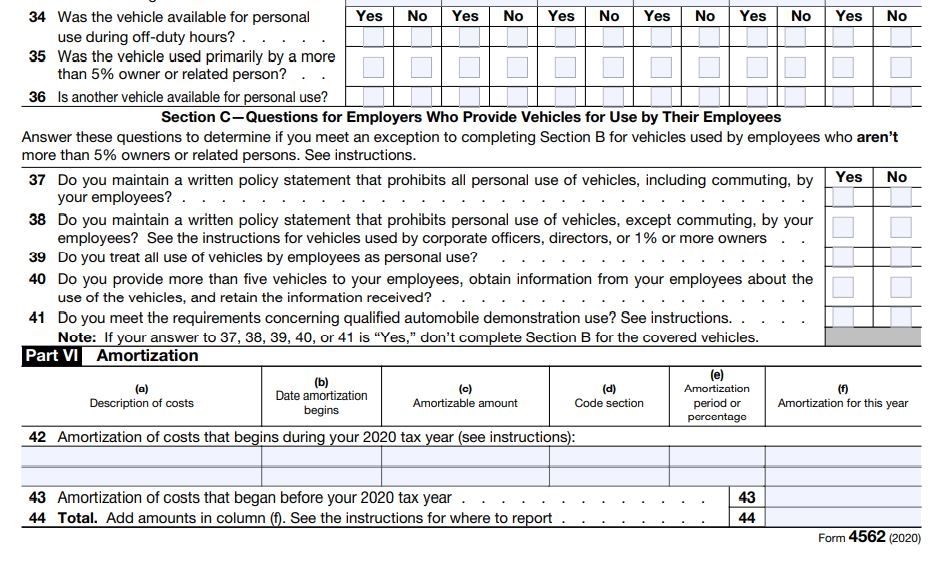

Part VI Intangible Assets Amortization

Which intangible assets are amortized?

How many years amortize intangible assets?

Certain Section 197 intangible properties are to be amortized over 180 months:

Business books and records

Patents

Copyright

Formula, pattern

Process

Permit, license, or right issued by a government

Franchise, trademark, trade name including renewal fees

Business startup cost

Organizational cost to create a corporation or a partnership

It is important you read page 15-16 of Instructions to Form 4562 Depreciation and Amortization if you need to amortize an intangible property. You would find the section code the intangible asset belongs to and how many months you should amortize it.

The code section is entered in column D for the intangible property you placed in service during the tax year.

Line 42 is for intangible property placed in service in the year you are filing for.

Line 43 is for intangible properties placed in service in prior years

Line 44 is the total amortization deduction for the year for line 42 and 43.

You only complete form 4562 Depreciation and Amortization for the first year you placed an intangible property in your business. For the remaining years, you would claim the amortization deduction directly on your business tax return. You don’t need to complete Form 4562 Part VI. But if you placed an asset in service for the first time, you would complete Form 4562 for that year and any amortization for intangible asset placed in service in prior years, would go on line 43.

If you have a C Corporation, you would submit Form 4562 every year along with your business tax return Form 1120 for all depreciation deduction whether a new asset is placed in service for the first time or not.

[/vc_column_text][/vc_column][/vc_row][vc_row css=”.vc_custom_1613990731336{margin-top: 10px !important;margin-bottom: 10px !important;}”][vc_column][vc_row_inner][vc_column_inner][tagline_box call_text=”2020 Federal Tax Forms and Instructions” call_text_small=”Save time and find the links to the right IRS Tax Form and Instructions for your business.” title=”Links to Tax Forms” target=”_blank” color=”custom” custom_bg_color=”#ebf3fb” custom_title_color=”#000000″ custom_description_color=”#000000″ button_text_color=”#000000″ button_border_color=”#c2ccf7″ button_bg_color=”#c2ccf7″ href=”https://ninasoap.com/categories/2020-federal-tax-forms-and-instructions/”][/vc_column_inner][/vc_row_inner][/vc_column][/vc_row][vc_row css=”.vc_custom_1613990731336{margin-top: 10px !important;margin-bottom: 10px !important;}”][vc_column][vc_row_inner][vc_column_inner][vc_video link=”https://youtu.be/Aay9is2Vb_A” el_width=”50″ el_aspect=”43″][/vc_column_inner][/vc_row_inner][/vc_column][/vc_row][vc_row css=”.vc_custom_1613990731336{margin-top: 10px !important;margin-bottom: 10px !important;}”][vc_column][vc_row_inner][vc_column_inner][vc_cta h2=”How do You Depreciate a Business Asset?” h2_font_container=”color:%23000000″ h2_google_fonts=”font_family:Spirax%3Aregular|font_style:400%20regular%3A400%3Anormal” h4=”Articles and videos to assist you claim the right depreciation deduction on your business assets.” h4_font_container=”color:%23000000″ h4_google_fonts=”font_family:Tauri%3Aregular|font_style:400%20regular%3A400%3Anormal” style=”custom” add_button=”right” btn_title=”Previous Articles” btn_style=”custom” btn_custom_background=”#5bc98c” btn_custom_text=”#000000″ use_custom_fonts_h2=”true” use_custom_fonts_h4=”true” h2_link=”url:https%3A%2F%2Fninasoap.com%2Fcategories%2Fhow-do-you-depreciate-a-business-asset%2F|title:How%20do%20You%20Depreciate%20a%20Business%20Asset||” h4_link=”url:https%3A%2F%2Fninasoap.com%2Fcategories%2Fhow-do-you-depreciate-a-business-asset%2F|title:How%20do%20You%20Depreciate%20a%20Business%20Asset||” custom_background=”#d5e8f2″ custom_text=”#000000″ btn_link=”url:https%3A%2F%2Fninasoap.com%2Fcategories%2Fhow-do-you-depreciate-a-business-asset%2F|title:How%20do%20You%20Depreciate%20a%20Business%20Asset||”][/vc_cta][/vc_column_inner][/vc_row_inner][/vc_column][/vc_row][vc_row css=”.vc_custom_1613990731336{margin-top: 10px !important;margin-bottom: 10px !important;}”][vc_column][vc_row_inner][vc_column_inner][tagline_box call_text=”Instant Digital Products” call_text_small=”Downloads you need to successfully manage your finances and your business” title=”Get What You Need When You Need It!” target=”_blank” color=”custom” custom_bg_color=”#008000″ custom_title_color=”#ffffff” custom_description_color=”#ffffff” button_text_color=”#000000″ button_border_color=”#ffd700″ button_bg_color=”#ffd700″ href=”https://liberdownload.com”][/vc_column_inner][/vc_row_inner][/vc_column][/vc_row][vc_row css=”.vc_custom_1613990731336{margin-top: 10px !important;margin-bottom: 10px !important;}”][vc_column][vc_row_inner][vc_column_inner][vc_wp_text]

Disclaimer:

“I am not an attorney to practice law. I am not allowed to draft legal documents, give advice on legal matters including immigration, or charge a fee for these activities.” Our articles are informative and based on our knowledge and experience. Use them at your own discretion.

Affiliate Links Disclaimer:

Our articles contain affiliate links. When you click on one of our affiliate links and make a purchase, we will receive a commission. We thank you very much for your support!

Please Find About our Products and Links Below

Free Download

Would you please check the “Free Download” section on our website for budget spreadsheet, budget planner PDF, tax forms, motivational quotes, checklists, and more for you do download. You don’t need to subscribe to access them. We would like to have you in our community where we interact and encourage each other to reach our goals. We invite you to join our email list.

https://ninasoap.com/free-downloads/

Our Objectives

At Nina’s Soap (Liberman Consulting L.L.C.), you would find information to live a quality life within budget and increase your net worth. Topics covered include personal finance, investment, business management, cooking from scratch and growing some vegetables and fruit to save money and eat healthy.

For more, would you please check our blog:

Contact Information: care@ninasoap.com

You Tube Channel:

https://www.youtube.com/c/LibermanConsultingLLC

Liberman Consulting L.L.C. Podcast:

Liberman Consulting L.L.C. Podcast (buzzsprout.com)

Join Us for Free

You are invited to join us where you could ask questions, stay motivated and work toward reaching your financial goals.

How to Find Previous Articles

To make it easy to navigate our website, would you please check the side bar? Under “Post Archives”, are our “categories”. The links to our prior articles are saved under their appropriate categories. Would you please click on any category under “Post Archives” to read the titles of previous articles and click on the link of your interest to open the article.

Welcome to Our Financial Success Group!

To learn more tips on how to live below your income without sacrificing the quality of your life and start building wealth, would you please join our community for FREE by subscribing here:

https://ninasoap.com/membership-join/

Our Online Stores

Welcome to Nina’s Soap our Natural Products Store

Our lye soaps are handmade with quality grade natural oils and butters, food grade sodium hydroxide, and herbs grown in our garden without pesticide or chemical fertilizer—- no additives, no fragrance, no dye.

Our towels, washcloths, and napkins are natural and eco-friendly alternatives of paper towels, paper napkins, and tissue papers for you to enjoy in the comfort of your home while saving money and the environment.

Welcome to Liber Label our Apparel Store

Customs design clothing, home décor, accessories, and stationery with motivational quotes to lift your mood every day.

Welcome to LiberOutlet.com our Resale Store

New and used toys, small kitchen appliances, household products, office supplies, packaging supplies at a bargain price.

Welcome to Liberdownload.com, Digital Products Store

Budget and Monthly Expense Tracker, Checklist to create your online store, Inventory and Sales Excel Template…tools you need to manage your money, start and run your business successfully, and reach your financial success.

Affiliate Links:

Bluehost: We host our websites at Bluehost and like their service. They take the time over the phone to help solve website issues

https://www.bluehost.com/track/ninasoap/

Please Register for Free

Registration

[/vc_wp_text][/vc_column_inner][/vc_row_inner][/vc_column][/vc_row]